Buying a home in Italy is often a lifestyle decision, but for many international families it is also a long-term estate planning decision. Understanding how inheritance tax works in Italy can therefore be useful before purchasing a second home or family property.

Italy is often seen as a complex country from a tax point of view. However, when it comes to inheritance tax for spouses and children, the Italian system can be more favourable than many international buyers expect.

This article explains the main inheritance tax rules in Italy, how they compare with other European countries, and which additional taxes may apply when inheriting Italian real estate.

For a broader overview of the purchase process, you can also read our guide to Buying in Italy.

How Italian inheritance tax works for spouses and children

In Italy, inheritance tax depends on the relationship between the deceased person and the heir. For transfers in favour of a spouse or direct relatives, such as children, parents or grandchildren, the inheritance tax rate is 4%. However, each beneficiary has a personal allowance of Euro 1.000.000.

This means that if a parent leaves assets worth up to Euro 1.000.000 to one child, no Italian inheritance tax is due on that transfer. The 4% tax applies only to the amount exceeding that threshold.

For example, if a child inherits Euro 1.200.000 from one parent, the taxable amount would generally be Euro 200.000, with inheritance tax calculated at 4% on that excess amount.

Italy compared with other European countries

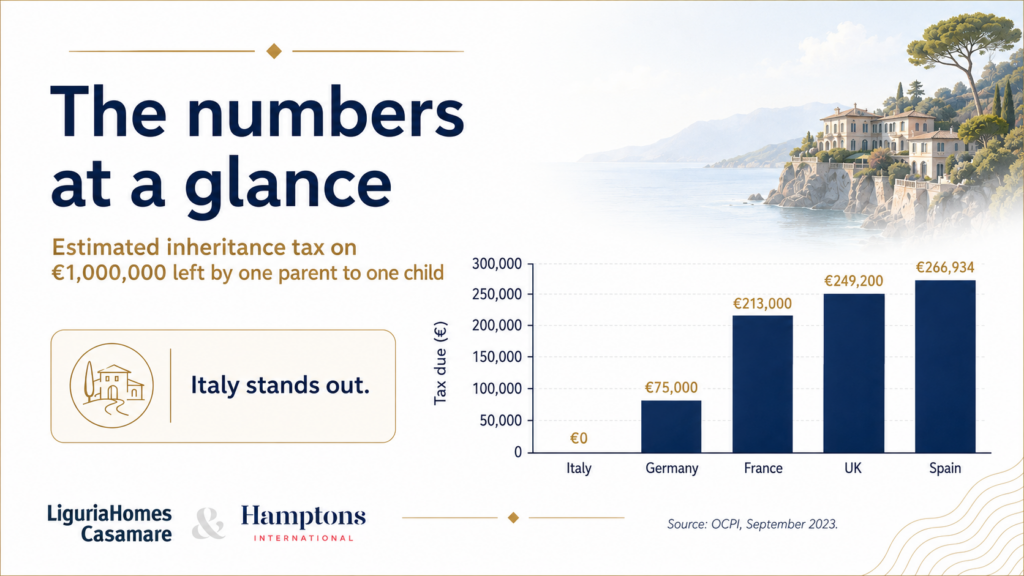

A 2023 analysis by OCPI, the Observatory on Italian Public Accounts, compared inheritance tax in several European countries using a simple example: Euro 1.000.000 left by one parent to one child.

The estimated inheritance tax was:

- Italy: Euro 0

- Germany: Euro 75.000

- France: Euro 213.000

- United Kingdom: Euro 249.200

- Spain: Euro 266.934

This comparison does not mean that Italy has no inheritance tax in every situation. It means that, in this specific example, the Italian allowance for direct heirs is high enough to avoid inheritance tax completely.

For international buyers purchasing a second home or family property in Italy, this is an important point to understand.

Why this matters for UK, Irish and Scandinavian buyers

For UK buyers, inheritance tax is often a key planning issue. In the United Kingdom, inheritance tax is generally charged at 40% on the part of the estate above the available tax-free threshold, although allowances and reliefs may apply.

For Irish buyers, the Irish Capital Acquisitions Tax system should also be considered. Gifts and inheritances received by children from parents benefit from a specific threshold, but tax may apply above that amount.

Scandinavian buyers have different starting points. Sweden and Norway do not currently have inheritance tax, while Denmark still applies estate taxation in certain cases.

This is why each buyer’s country of residence and personal situation matter. A property located in Italy will require Italian succession formalities, but the buyer’s home country rules may also be relevant.

International buyers should also consider the tax rules of their country of residence, as cross-border inheritance situations may involve more than one jurisdiction.

Inheriting property in Italy: other taxes to consider

A common misunderstanding is to think that if no Italian inheritance tax is due, there are no costs at all. That is not correct.

When an estate includes Italian real estate, other property-related taxes are normally due, even if inheritance tax itself is not payable because of the Euro 1.000.000 allowance.

The main taxes are:

- Imposta ipotecaria, mortgage tax, generally 2% of the cadastral value of the property.

- Imposta catastale, cadastral tax, generally 1% of the cadastral value of the property.

These taxes are connected to the transfer and registration of the property in the Italian land and cadastral registers.

If the heir qualifies for Italian “prima casa” benefits, these taxes may be reduced to fixed amounts, generally Euro 200 each. This must always be verified with a notary or qualified tax adviser.

There may also be administrative charges, stamp duties and professional fees connected to the succession declaration.

Continue reading Buying Property in Italy and Inheritance Tax: a Guide for International Buyers